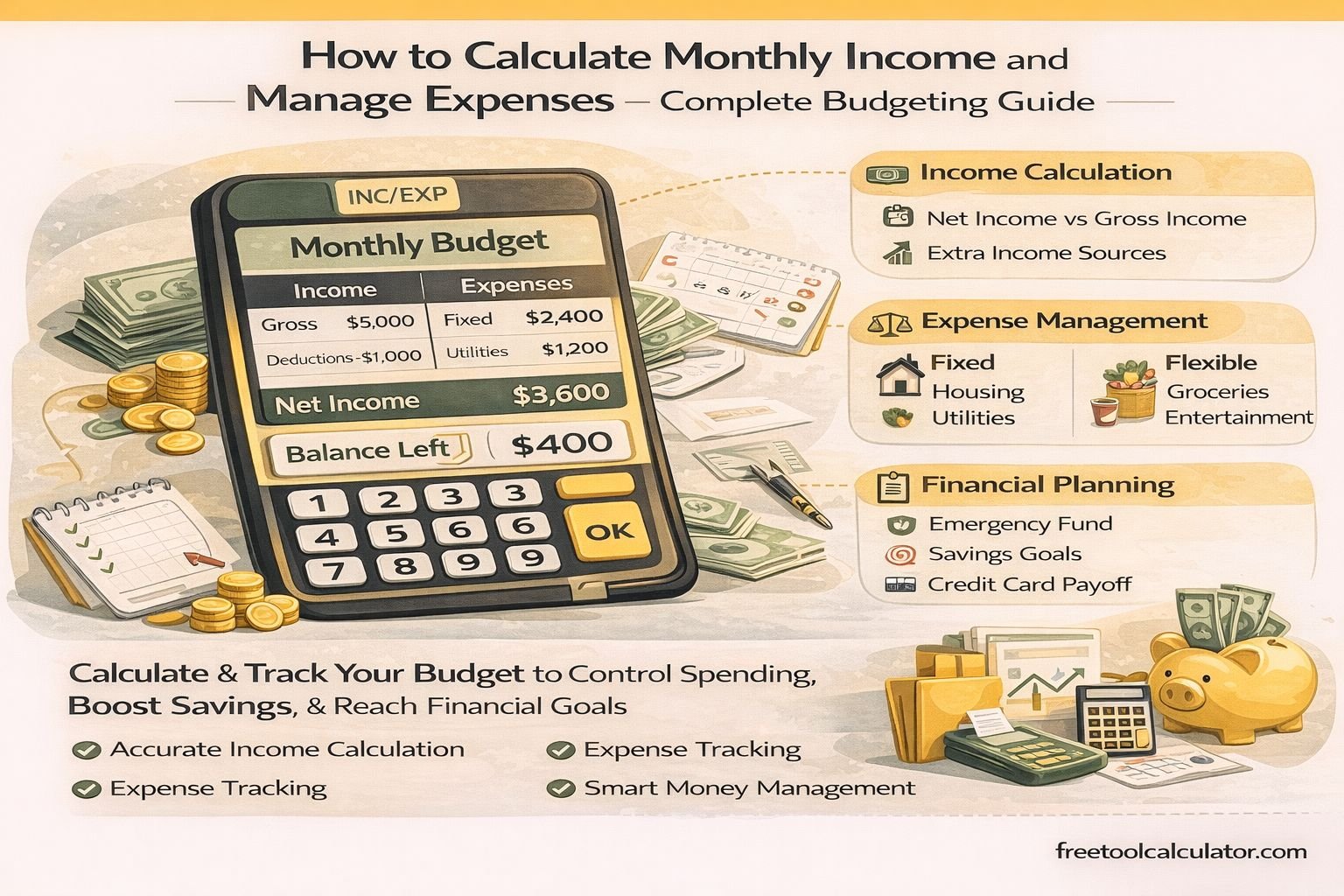

How to Calculate Monthly Income and Manage Expenses Effectively

Managing your finances starts with understanding how much you earn and how you spend it. A well-structured budget calculator helps you track income, categorize expenses, and make informed financial decisions. Whether your income is stable or fluctuating, knowing how to calculate monthly income, use net income correctly, and differentiate between fixed and flexible expenses is essential for financial stability. In this complete budgeting guide, you will learn practical methods to manage your money effectively and build a sustainable financial plan.

How to Calculate Monthly Income If It Varies

For individuals with irregular income such as freelancers, business owners, or commission-based professionals, calculating a stable monthly income can be challenging. Instead of relying on a single month, the best approach is to calculate your average monthly income.

Step-by-Step Method

Start by adding your total income over the past 6 to 12 months. Then divide that total by the number of months.

Formula:

Average Monthly Income = Total Income ÷ Number of Months

Example

If your total income over 12 months is $36,000, your average monthly income would be $3,000.

This approach smooths out fluctuations and provides a reliable baseline for budgeting. For better accuracy, always use a longer time frame such as 12 months, especially if your income varies seasonally.

You can simplify this process using a budget calculator to automatically compute your average income and align it with your expenses.

Best Practices for Variable Income Budgeting

– Use conservative estimates based on lower-income months

– Maintain an emergency fund to handle income gaps

– Recalculate your average income regularly

– Separate essential and non-essential expenses clearly

These strategies ensure better financial control and reduce the risk of overspending during low-income periods.

Gross Income vs Net Income – Which One Should You Use?

Understanding the difference between gross income and net income is fundamental in personal finance and budgeting.

What Is Gross Income?

Gross income refers to your total earnings before deductions such as taxes, insurance, or retirement contributions.

What Is Net Income?

Net income is your take-home pay after all deductions. This is the actual amount available for spending and saving.

Why Net Income Is Better for Budgeting

When creating a budget, always use net income because it reflects your real financial capacity. Using gross income can lead to overestimating your available funds, resulting in poor financial decisions.

Net income ensures:

– Accurate expense planning

– Better savings allocation

– Reduced financial stress

– Realistic budgeting goals

When Gross Income Is Useful

Gross income is still relevant for tax calculations, salary negotiations, and loan applications. However, it should not be used for daily budgeting or expense tracking.

A structured budget planning tool helps you work with net income to generate accurate financial insights.

Understanding Fixed and Flexible Expenses

A key part of effective budgeting is categorizing your expenses into fixed and flexible costs. This classification helps you identify where your money goes and where you can make adjustments.

Fixed Expenses

Fixed expenses are consistent, recurring costs that do not change significantly each month.

Examples include:

– Rent or mortgage payments

– Insurance premiums

– Loan repayments

– Subscription services

Characteristics:

– Predictable and stable

– Mandatory payments

– Difficult to reduce quickly

Flexible Expenses

Flexible expenses, also known as variable expenses, fluctuate based on your lifestyle and spending habits.

Examples include:

– Groceries

– Dining out

– Entertainment

– Shopping

– Travel

Characteristics:

– Adjustable and controllable

– Vary month to month

– Offer opportunities for savings

Why This Classification Matters

Separating fixed and flexible expenses allows you to:

– Prioritize essential spending

– Identify unnecessary expenses

– Improve savings strategies

– Maintain better financial discipline

Flexible expenses are where most cost-cutting opportunities exist, making them a critical focus area in any budgeting strategy.

How to Build a Simple Monthly Budget

Creating a monthly budget involves organizing your income and expenses into a structured plan.

Basic Budget Formula

Budget = Net Income − Total Expenses

Steps to Create a Budget

1. Calculate your net monthly income

2. List all fixed expenses

3. Estimate flexible expenses

4. Subtract expenses from income

5. Adjust spending to maintain a surplus

A positive balance indicates savings, while a negative balance highlights the need to reduce expenses.

Using an automated budget calculator simplifies these steps and provides instant results.

Common Budgeting Mistakes to Avoid

Many people struggle with budgeting due to common mistakes that reduce financial efficiency.

These include:

– Using gross income instead of net income

– Ignoring irregular expenses

– Underestimating flexible costs

– Not tracking spending regularly

– Failing to adjust the budget over time

Avoiding these mistakes helps maintain a realistic and effective financial plan.

Practical Tips for Better Financial Planning

Improving your financial health requires consistent effort and smart decision-making.

Key tips include:

– Track every expense regularly

– Set clear savings goals

– Reduce unnecessary spending

– Build an emergency fund

– Review your budget monthly

These practices enhance financial awareness and support long-term stability.

Why You Should Use a Budget Calculator

Manual budgeting can be time-consuming and prone to errors. A digital tool simplifies the process and improves accuracy.

Benefits of using a budget calculator include:

– Automatic calculations

– Clear income vs expense breakdown

– Better financial insights

– Time-saving process

– Improved decision-making

A reliable budget calculator tool ensures that your financial planning is accurate, efficient, and easy to manage.

Conclusion

Understanding how to calculate monthly income, choose between gross and net income, and manage fixed and flexible expenses is essential for effective budgeting. These core financial principles help you create a realistic plan, control spending, and increase savings.

By using structured methods and reliable tools, you can take full control of your finances and build a secure financial future. Consistent budgeting is not just about tracking money—it is about making smarter financial decisions every day.